Internal controls often sit in the background of a purchasing program, but they’re the quiet machinery that keeps everything honest.

These management-defined processes, rules, and checks promote accountability and prevent fraud. In purchasing, they guide spend toward authorized vendors, keep approvals within policy, and create a trackable record of every decision.

Strong controls don’t slow teams. They give people a structure they can trust, so decisions are faster, cleaner, and easier to defend. When they’re missing or inconsistent, small mistakes snowball into compliance problems, reporting gaps, and financial exposure.

Why purchasing internal controls matter for financial integrity

Internal controls shape every purchasing decision that follows: what gets bought, who approves it, how it’s recorded, and whether leadership can rely on the numbers later.

Here’s what strong controls prevent:

1. Rogue and unauthorized spend

Controls keep purchases tied to approved vendors, budgets, and policies, so staff can’t bypass the process or create commitments the organization didn’t plan for.

2. Unapproved invoices and duplicate payments

Invoice controls catch mismatches early and ensure every invoice corresponds to a legitimate order, preventing errors that inflate costs and drain time.

3. Incorrect cost allocations

Coding requirements at the point of request keep expenses tied to the right project, grant, or department, so reporting stays precise and audits move faster.

4. Fraud attempts and bad faith activity

Separation of duties, approval thresholds, and audit trails make it harder for suspicious activity to slip through unnoticed.

5. Spend leakage and off-contract buying

Built-in vendor rules keep teams within negotiated pricing and preferred suppliers, helping organizations avoid small but steady losses over time.

6. Reporting gaps and audit findings

Consistent control leaves a complete record of who approved what, when, and why, reducing the scramble for documentation when auditors start asking questions.

Organizations don’t invest in purchasing internal controls for the sake of procedure. They do it because they protect financial integrity exactly where money leaves the business. They’re the backbone of strategic and accountable purchasing.

What strong internal controls look like in practice

Strong purchasing controls don’t live in a policy binder. They manifest in the way work moves through the system day after day. The organizations that excel at purchasing follow a handful of best practices:

Segregation of duties

When requesting, approving, and paying sit with different people, it becomes much harder for mistakes or misuse to slip through. This separation creates natural checks and balances in the workflow.

Documented workflows

When the purchasing process is written clearly and kept up to date, people know what the right steps look like and can follow them without improvising. Documentation removes guesswork and keeps approvals, timelines, and responsibilities steady across departments.

A single source of truth for all purchases

Controls work best when all requests, comments, and approvals land in one place instead of getting scattered across inboxes and spreadsheets. Centralizing the trail speeds up the reporting and gives finance a reliable view of what’s been committed.

Automation keeping every purchase on the right track

Routine checks shouldn’t rely on memory. Procurement software solutions handle the repetitive work, route requests to the right people, and flag anything that needs attention.

Policies people can follow, and systems can enforce

Simple, practical guidelines make compliance easier. When policies are clear and tied directly to how the system works, staff understand what’s expected and the software reinforces those expectations.

Continuous evaluation

Strong controls evolve with the organization. Regular reviews help teams spot gaps, update rules, and adjust workflows as needs change. This steady maintenance keeps the entire purchasing cycle stable and prevents issues from slipping in over time.

.png?width=1440&height=356&name=Call%20To%20Action%20-%20Gradient%20-%20OPTION%201.2%20(1).png)

Purchasing software features that enable financial transparency and proactive control

Manual controls can only carry an organization so far. Paper trails get lost, approval paths drift, and the effort required to keep everything aligned pulls people away from real work.

The controls below show how digital structure protects both accuracy and accountability.

1. Clear division of responsibilities that prevents conflicts and fraud

Strong systems separate who requests, who approves, and who records the payment. This simple split limits the chance of inappropriate approvals and protects the organization from intentional or accidental misuse.

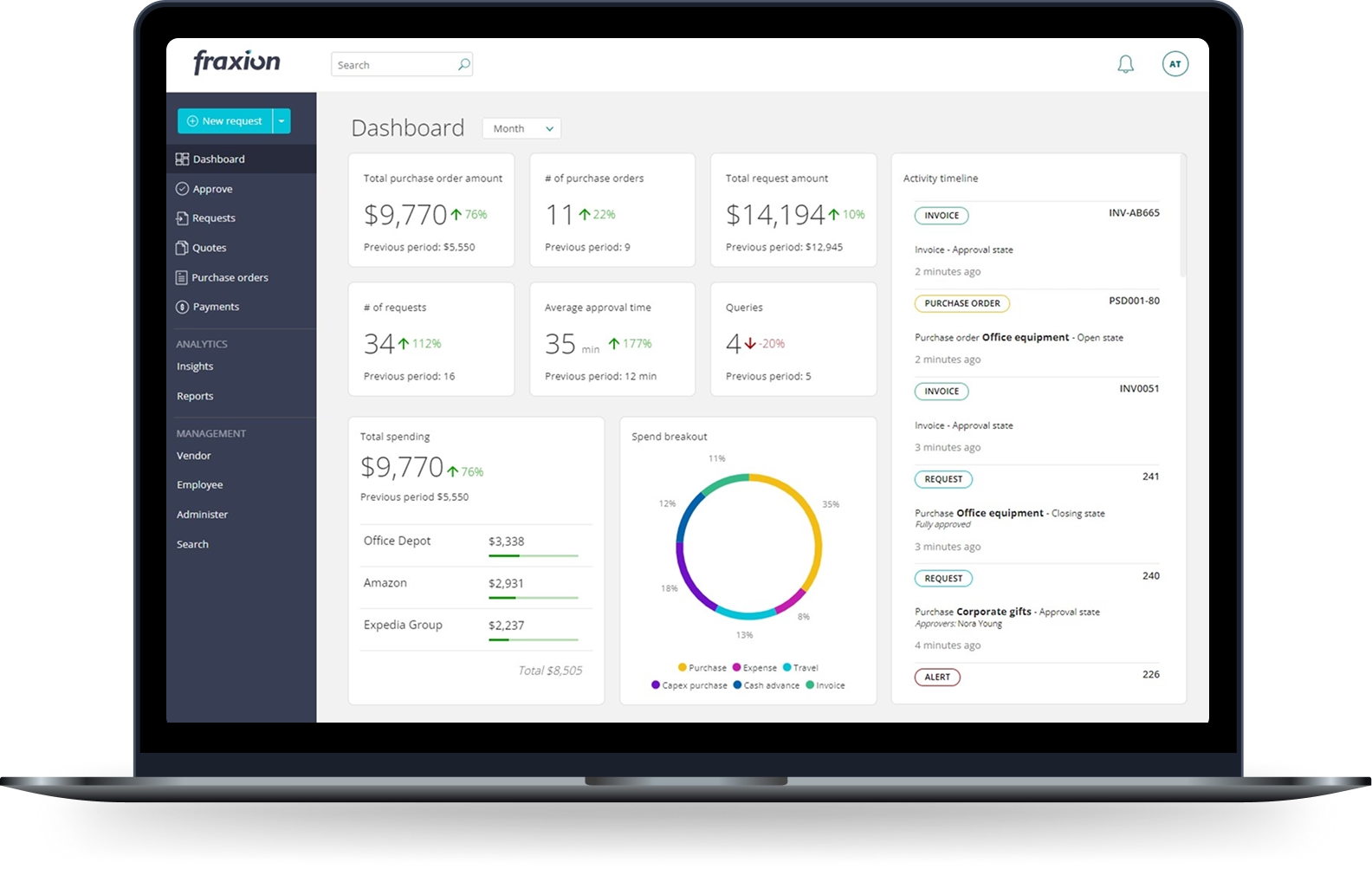

Fraxion supports this setup with configurable roles and approval paths that keep responsibilities distinct and traceable.

2. Approval rules that enforce accountability at every step

Clear rules keep decisions consistent. When thresholds, vendor lists, and routing logic are built directly into the system, approvals follow the same pattern every time. Staff know what to expect, and managers can see why a request moved the way it did.

Fraxion’s automated workflows guide each request through the right people without back-and-forth emails.

3. 3-way matching without the manual downtime

Matching the order, invoice, and receipt is one of the most effective controls, but doing it by hand is time-consuming and labor-intensive.

Fraxion streamlines this step by using AI-powered invoice capture and automated routing to pull the documents into one record and surface only the exceptions that need attention.

4. Accurate cost allocation for clean, trusted reporting

Clean reporting depends on correct coding. When requesters choose the right cost center or project at the start of the process, finance doesn’t have to fix errors later. Systems that guide people to the right allocation reduce rework and produce reports leaders can trust.

Fraxion reinforces this accuracy by linking each transaction to a budget line as it enters the workflow.

5. Detective controls that uncover issues early

Detective controls find errors or problems after the transaction has occurred. These controls are essential because they provide evidence that preventive controls are operating as intended, as well as offer an after-the-fact chance to detect irregularities. Regular checks on spending behavior, exception logs, and audit alerts help finance teams spot unusual activity early.

With system-generated visibility, Fraxion makes these reviews simpler by collecting all supporting details in one record.

6. Audit trails that make accountability effortless

Every purchasing step should leave a clean footprint. When systems automatically record who approved what, when, and why, teams stop scrambling during audits.

Fraxion maintains this trail in the background, so accountability isn’t something people have to remember to record.

How Fraxion builds internal control into every purchase

- Builds structure into every step. Approvals follow the right path automatically, budgets show up before anyone commits to spend, and requests can’t skip the checks that keep the process clean.

- Keeps records complete without extra work. Each transaction carries its own audit trail—who approved what, when, and why—so reviews move faster and examiners get the full picture without follow-up rounds.

- Enforces policy consistently. Thresholds, vendor rules, allocations, and funding restrictions stay tied to the workflow, making the right decision easier than the workaround.

- Catches issues early. The system flags mismatches, over-budget requests, or out-of-policy activity as it happens, giving teams a chance to correct the problem before it turns into a reportable exception.

If you want to see what these controls look like in practice, you can book a demo and we will walk through a real purchasing cycle inside Fraxion.

FAQs